Effect of Loan Loss Provisions on Financial Stability and Profitability of Banks

DOI:

https://doi.org/10.63056/lsjmiss.1.4.2025.146Keywords:

Loan Loss Provisions, Financial Stability, Profitability, Banks, Credit Risk, PakistanAbstract

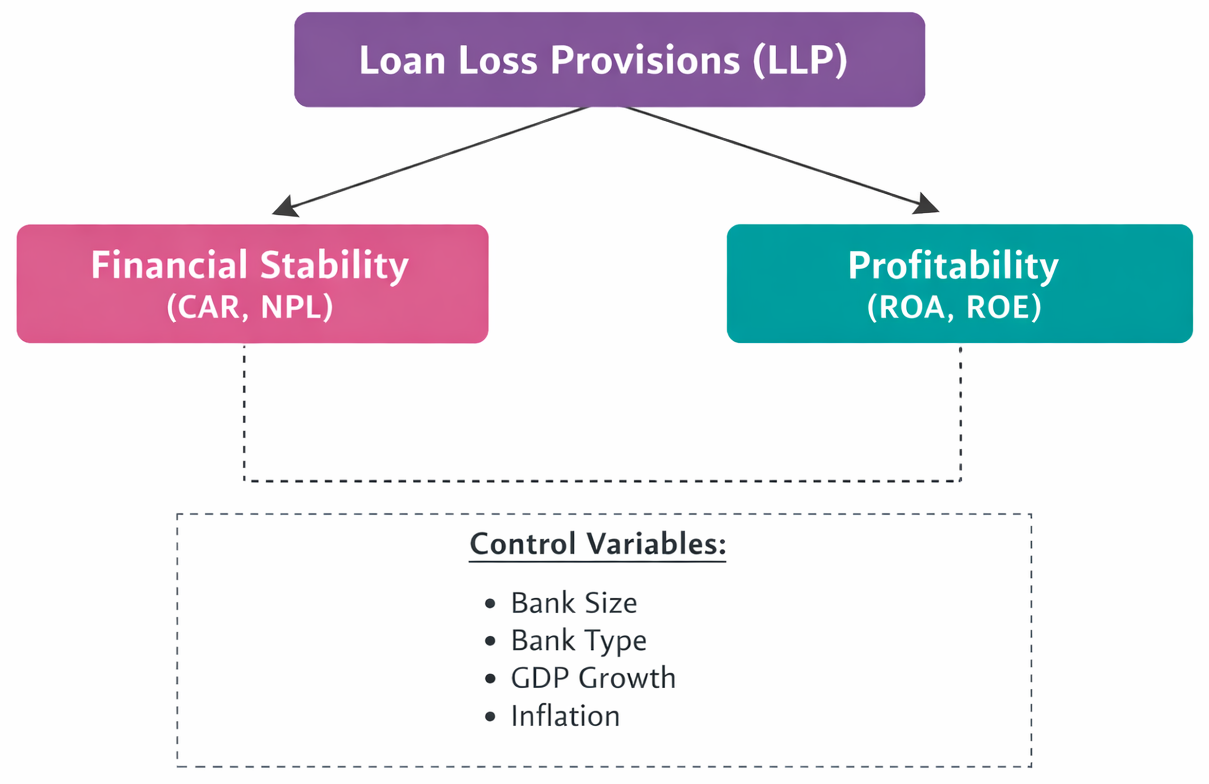

Loan loss provisions (LLPs) play a crucial role in the banking sector by serving as financial buffers against potential losses arising from non-performing loans and credit risk. This study examines the effect of loan loss provisions on the financial stability and profitability of commercial banks in Pakistan. Grounded in the Prudential Regulation Theory and the Risk-Adjusted Performance framework, the study investigates how provisioning practices influence banks’ capital adequacy and earnings performance. A quantitative research design is employed using panel data from commercial banks listed in Pakistan over a ten-year period (2013-2022). Secondary financial data are collected from bank annual reports, State Bank of Pakistan publications, and financial databases. Descriptive statistics, correlation analysis, and panel regression techniques are applied to analyze the relationships between LLPs, financial stability indicators (capital adequacy ratio and non-performing loans), and profitability measures (return on assets and return on equity). The findings indicate that higher loan loss provisions significantly enhance financial stability by strengthening capital buffers and reducing credit risk exposure. However, increased provisioning negatively affects short-term profitability due to its direct impact on earnings. The study highlights the trade-off between risk management and profit maximization and provides policy implications for bank management and regulators to ensure sustainable financial performance.

Downloads

Published

How to Cite

Issue

Section

License

Copyright (c) 2025 Muhammad Naeem Shah, Dr. Muhammad Sadiq Shahid

This work is licensed under a Creative Commons Attribution 4.0 International License.